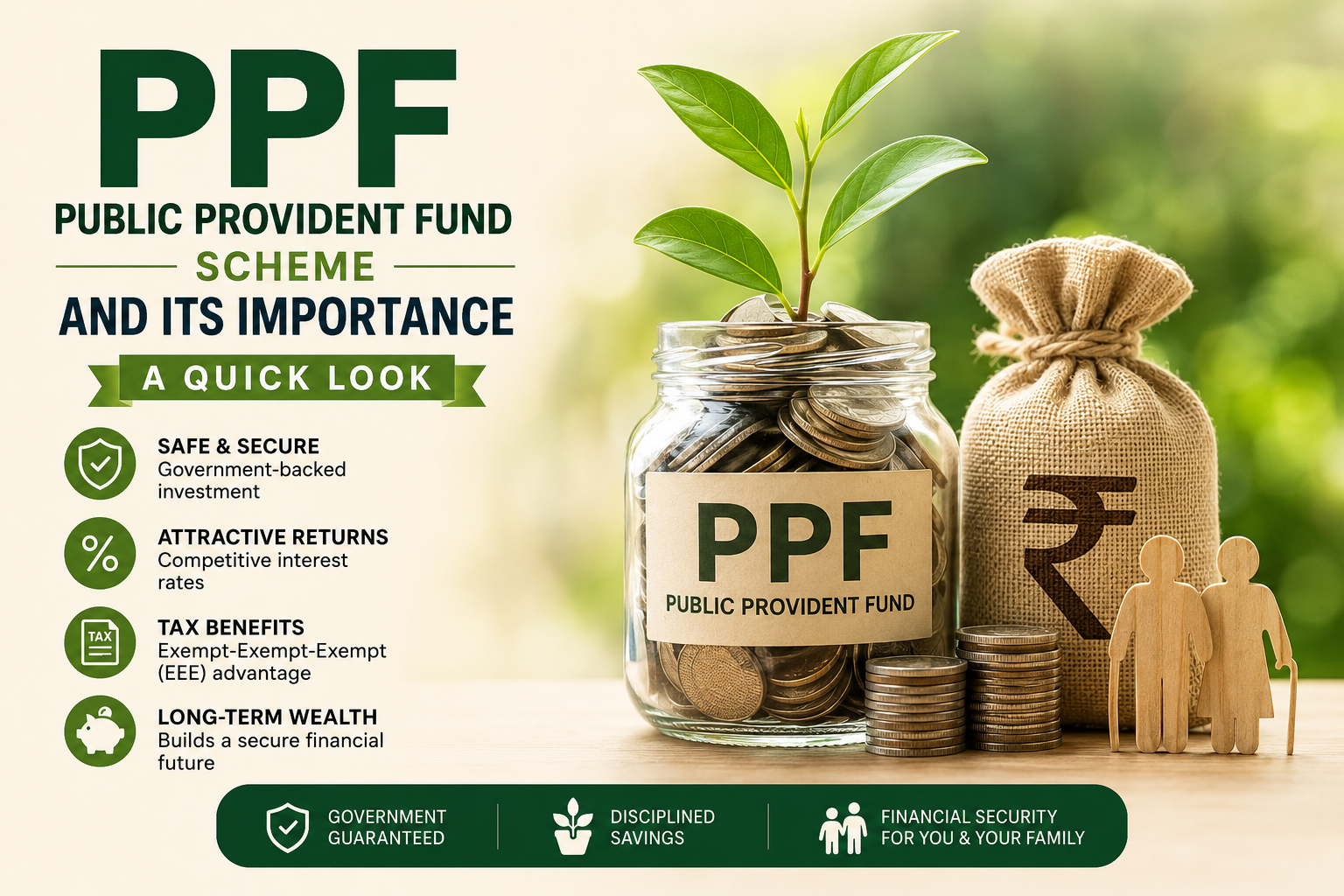

One of the most popular government investment tools, the public provident fund scheme, was launched way back in 1968 by the National Savings Institute of the Ministry of Finance. Introduced to provide financial security to its citizens, this scheme offers a combination of security, competitive interest rates and tax benefits – making it a valued investment tool for millions seeking to build a secure financial future.

Over time, the PPF has emerged as a powerful tool to create long-term wealth for investors. It is also one of the favoured investment options to accumulate a retirement corpus.

Why is the PPF Scheme so popular?

Since the public provident fund is a near-zero risk investment, it makes it an ideal choice for risk-free investors. Also, it is one of the safest investment options as the returns are guaranteed by the government of India. The central government sets the interest rate every quarter. The PPF scores over other forms of investment tools mainly because the overall investment is exempted from tax under Section 80C of the Income Tax Act, and even the returns on PPF are also not taxable.

PPF Account Features

A common government investment option, the PPF account comes with multiple features like low investment amount, flexible investment options and even tax benefits. Let’s take a quick look:

- Investment Limits: This is one of the most lucrative aspects of a PPF account – you can begin your investment with only Rs. 500 in a financial year, which amounts to a mere Rs. 42 per month. As far as the maximum limit is concerned, you can deposit up to Rs. 1.5 lakhs a year.

- Tenure: A PPF account comes with a minimum lock-in period of 15 years. However, the maturity date can be more than 15 years. Why? Because the 15-year maturity period of a PPF account is calculated from the end of the financial year in which the first investment was made. Also, a PPF account can be further extended in blocks of 5 years, with or without contributions. So, you can continue to enjoy the benefit of PPF for 20 years, 25 years, 30 years, and so on.

- Nomination Facility: A PPF account comes with nomination facilities where you can add one or more individuals as a nominee to your account.

- Risk Factor: It is a fully government-run scheme offering fixed returns, hence it is considered a safe investment tool with near-zero risk.

- Mode of Deposit: You can deposit in a PPF account offline or online. You can deposit offline by cash, cheque, or a demand draft (DD). In online mode, you can directly transfer via net banking or mobile banking facility.

- Frequency of Deposit: There no limit on frequency of deposits in this account. You can make any number of instalments. However, in order to keep the account active, you must deposit Rs.500 annually without fail.

- Opening Balance: You can open a PPF account with a minimum opening balance of Rs 100. However, you must deposit Rs 500 per financial year to keep it active.

Tax Benefits of the PPF Scheme

Investors usually prefer the Public Provident Fund Scheme because of its tax-exempt nature. So, the answer to whether PPF is taxable is a big NO.

The first exemption is on the deposits you make in a PPF account. Deposits to a PPF account are exempted from the taxation up to a maximum of Rs. 1.5 lakh in a FY under Section 80C of the Income Tax Act, 1961. A Tax saving fixed deposit has a higher interest-earning potential than savings accounts.

The second exemption on a PPF account is the interest earned on the deposits made annually. The interest earned are also tax free.

The third exemption of PPF scheme is on the received maturity amount. Once the amount matures after a span of 15 years, the maturity proceeds that you receive at withdrawal will also be exempted from tax. This makes a PPF account scheme a total Exempt-Exempt-Exempt (EEE) option.

The Last Words

Considering the EEE benefit offered by the PPF scheme, it is definitely one of the best investment tool for generating long-term savings. If you are a salaried individual, a self-employed person or an entrepreneur – you can always choose to invest in a public provident fund account and continue to reap benefits.

By Sampurna Majumdar

Sampurna Majumder is a communications professional born and raised in Kolkata. Fascinated by creativity from a young age, she has a deep love for music, literature, and world cinema. An avid reader and traveler, she holds a Master’s degree in Literature from the University of Delhi.

You have made the concept of PPF very easy to understand. Now I know its advantages. Thanks!

Thanks Richa

Appreciate the lucidity with which you elucidate financial terms and schemes…helpful indeed!

Thanks much Promita